Platforma do zarządzania funduszem VC/PE, onboardingu inwestorów, operacji kapitałowych oraz analityki portfela.

According to the definition set out in Article 8a of the Act on Investment Funds and the Management of Alternative Investment Funds, an AIF (Alternative Investment Fund) is an alternative investment fund other than a specialised open-ended investment fund or a closed-ended investment fund.

Pursuant to Article 8a(2), an Alternative Investment Company may operate in the form of:

The sole purpose of an AIF’s activities is to collect assets from multiple investors for the purpose of investing them in the interest of those investors, in accordance with a defined investment policy. Read more about the requirements for entry into the register of AIF managers.

We provide comprehensive services for private investment vehicles in the form of Alternative Investment Funds (AIFs), designed for the contribution of financial assets by high-net-worth individuals. Such AIFs emerged as an alternative during the absence of family foundation regulations and continue to offer strong predictability in the context of evolving legal frameworks for wealth management. In light of the still unclear plans of the Ministry of Finance regarding family foundations, an AIF provides a stable and secure solution for investors.

We serve most of the major private venture capital (VC) funds in Poland that operate as Alternative Investment Funds (AIFs). Such structures are usually limited to a small group of investors, which supports a more individual approach and better tailoring of the investment strategy. However, there are also funds that involve several dozen limited partners (LPs), enabling them to increase investment capital and carry out larger projects.

Our clients also include major public funds, such as Vinci AIF and PFR Ventures AIFs, which under the FENG program will operate as fund-of-funds, investing in AIFs within the FENG Starter, Biznest, Open Innovation, Koffi, and CVC programs.

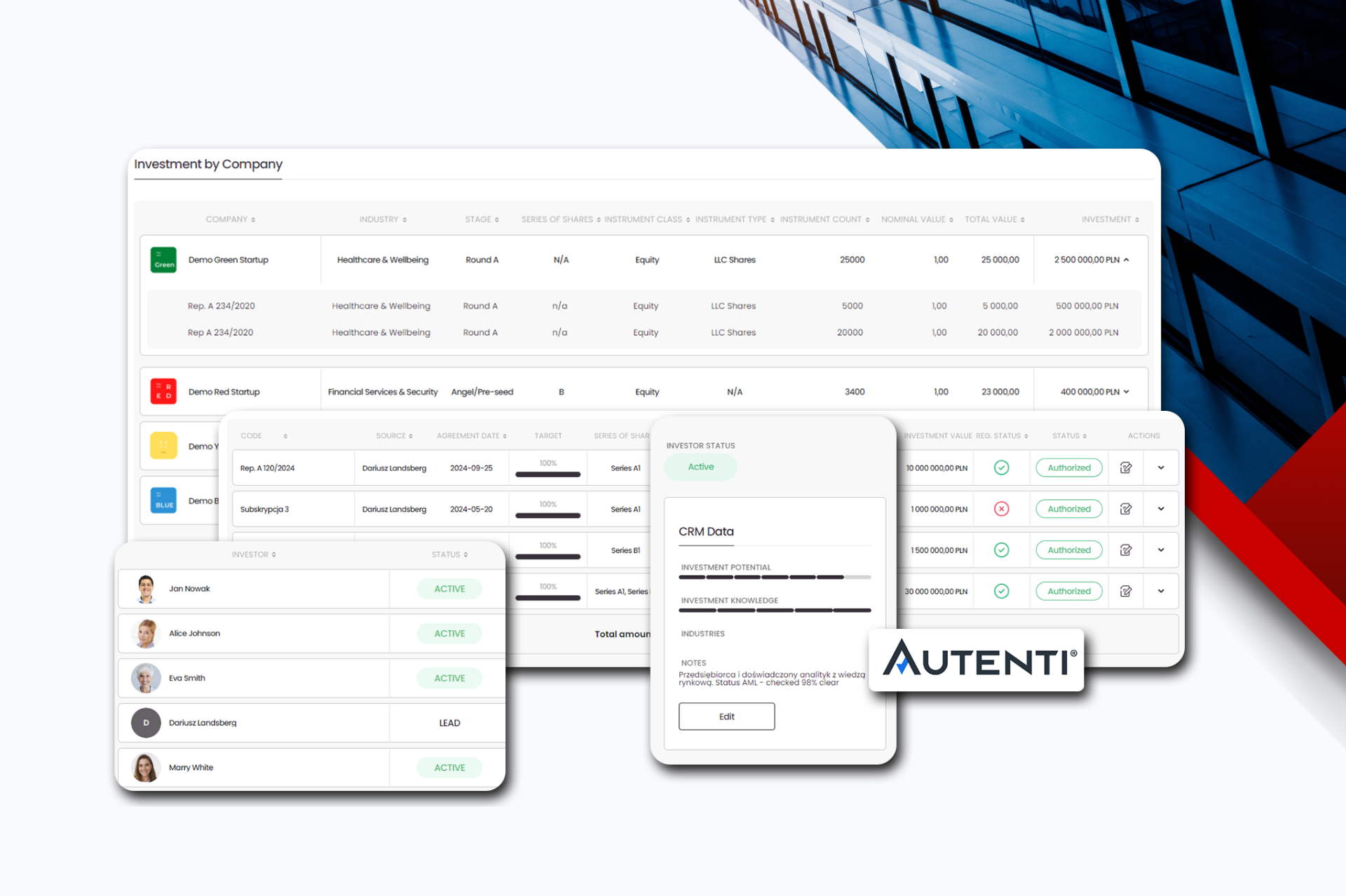

As the only entity on the market and AIF servicer with unmatched experience in servicing AIFs, we also support trading platforms operating in the form of AIFs, providing integration with platforms such as Interactive Brokers and the AIF’s accounting records, thereby giving AIF investors online access to the Investor Panel.

Genprox, using the Fundequate platform, is the only entity that has gained the trust of PFR Ventures and services licensed AIFs of PFR Ventures, which will be used for the distribution of funds under the FENG program.

Our expertise and experience in the investment fund market also enable us to provide comprehensive services for Investment Funds.

Since the introduction of the AIFMD Directive into the Polish legal framework, Genprox has been shaping the VC/PE fund market. Therefore, for the VC/PE funds we service in the form of an Alternative Investment Fund (AIF), we provide: a unified accounting policy, a consistent chart of accounts tailored to reporting specifics (regulatory reporting, financial statements, and management reporting), uniform criteria for revenue and expense recognition, as well as a standardized methodology for the classification of financial instruments and the valuation of AIF assets.. By applying a consistent data model for AIF portfolio companies, we also ensure efficient month-end and year-end closing without the need to aggregate and standardize data received from portfolio companies. Learn more about how to manage AIF accounting on the Fundequate platform. .

fundequate platform

Valuation of AIF assets and determination of net asset value (NAV), as well as the NAV per participation right, in accordance with the Accounting Act and Article 70h(1) of the Investment Funds Act. Genprox, pursuant to Article 70h(5), as an entity authorised to provide accounting services, qualifies as an external valuation entity (Article 70h(3)(2)). We offer the development and implementation of rules and procedures for the valuation of AIF assets, taking into account Articles 67–72 and Article 74 of EU Commission Regulation No. 231/2013.

Financial statements of an AIF, in accordance with the requirements of Article 45. the Accounting Act and Article 222d(4) of the Investment Funds Act, consisting of the balance sheet, the profit and loss account, the notes to the financial statements, the investment portfolio statement, and the statement of additional information on the structure of assets and operating costs, the net asset value and information on the net asset value per participation right and the method of its determination, as well as information on the financial instruments issued by the Alternative Investment Fund, in accordance with the Regulation of the Minister of Development and Finance of 12 December 2016 on the scope of information to be disclosed in the financial statements of AIFs.

We provide AIF managers with support in meeting regulatory requirements, i.e. periodic reporting in accordance with Article 222e(1) of the Amending Act, together with EU Commission Regulation No. 231/2013 and the Regulation of the Minister of Development and Finance of 9 December 2016 on supplementing the disclosure obligations of AIFMs. AIF accounting forms the basis of records, on which we ensure reporting to the KNF in accordance with Article 225(4) of the Amending Act, together with the Regulation of the Minister of Finance of 6 March 2018 on periodic reports and information concerning the activities and financial situation of AIF managers submitted to the KNF (structured XML file).

Focus on fundraising, scouting, and monitoring the investments of your fund. As for the setup, accounting, reporting, and taxation of VC/PE funds operating in the form of an Alternative Investment Fund (AIF) — we know it all. So leave that to us.

We are an accounting and advisory firm specializing in the accounting of AIFs. We possess broad professional expertise and hold certifications such as Investment Advisor, ACCA, and Tax Advisor. This enables the VC funds we serve to receive, in one place, a comprehensive service unavailable from any other accounting firm or law office. We specialize in servicing VC funds and have a deep understanding of their reporting needs. As a result, we are able to provide full accounting, tax, and reporting support for any type of VC/PE fund in Poland as well as for alternative funds in Luxembourg.

The accounting of an AIF must be conducted in accordance with Polish accounting standards and the provisions of the Accounting Act. In addition, many AIFs are subject to detailed regulations related to financial reporting and the valuation of investment assets.

Yes, Alternative Investment Funds (AIFs) are required to maintain full accounting records, which means keeping accounting books and preparing full annual financial statements, including the cash flow statement and the statement of changes in equity. In addition, AIFs are obliged to prepare an investment portfolio statement and supplementary information on the AIF. The financial statements of an AIF must then be audited by a statutory auditor.

The valuation of AIF assets must be carried out in accordance with applicable accounting regulations, which require the use of methods appropriate to the type of assets. An AIF is obliged to measure its assets at fair value.

AIFs are required to submit annual asset reports to the KNF. Preparing such reports requires specialist knowledge and precise handling of the DATMAN and DATAIF file structures, which must be submitted through the KNF’s ESPI system. Genprox specializes in this reporting to the KNF, servicing 70% of the assets under management by AIFs in Poland.

The most common challenges include: accurate valuation of investment assets, compliance with regulatory requirements, management of tax settlements, and reporting to the KNF. Support from a specialized firm such as Genprox can help avoid errors and ensure compliance with the regulations.

Yes, AIFs are required to have their financial statements audited annually by independent auditors. These audits are intended to confirm the accuracy and financial compliance of the company.

Alternative Investment Funds (AIFs) are subject to corporate income tax (CIT). However, in certain cases, they may benefit from an income tax exemption, provided that specific requirements are met.

Yes, specialized software enables the automation of accounting processes, asset valuation, and the generation of regulatory reports. Genprox uses the Fundequate platform, which supports the comprehensive financial management of AIFs.

AIFs are required to prepare annual financial statements in compliance with the Accounting Act. In addition, companies under the supervision of the KNF must regularly report their asset structure and financial flows.

To avoid errors, it is essential to use the services of professionals experienced in handling AIFs and to ensure regular updates on changing regulations. Genprox provides support in every aspect of AIF accounting, ensuring accuracy and compliance with regulations.

The required documents include, among others, the articles of association or partnership agreement of the AIF, an extract from the National Court Register (KRS), details of the management board members, and information from the National Criminal Register.

An AIF may operate in the form of a joint-stock company, a limited liability company, a European company (SE), or a limited joint-stock partnership.

The AIF manager should be registered under statistical code 66.30.Z – activities related to fund management.

The accounting office must ensure proper maintenance of accounting books in accordance with the Accounting Act and reporting to the Polish Financial Supervision Authority (KNF).

The investment policy should cover investment objectives, criteria for selecting assets, diversification rules, and investment risks.

It is required to verify investors as professional clients and to conduct an analysis of the origin of their funds.

The chart of accounts must be tailored to the specific nature of an AIF’s activities, taking into account the recording of fixed assets, investments, and liabilities.

Errors include, among others, incomplete data of management board members, missing documentation of the investment policy, and inconsistencies in the descriptions of the business activity.

The procedures include activities such as the sale of shares, the admission of new investors, and the increase of contributions by limited partners.

The obligations include regular financial reporting, maintaining accounting books in accordance with the Accounting Act, and complying with tax law regulations.